Forward Revenue Finance: Turning Supply Chains into Bankable Assets

A hardware company is not a firm. It is a temporary command structure sitting on top of a supply chain.

The firm has the logo, the customer relationship, the board deck, the working-capital line, and the purchase orders. The supply chain has the process memory. It knows which adhesive fails after humidity exposure, which casting geometry looks elegant but will never deburr cleanly, which operator step can be automated, which battery enclosure is safe on paper but hateful in production, and which supplier-of-a-supplier is about to become the real bottleneck.

The firm is legible to capital.

The supply chain is legible to production.

That mismatch is one of the reasons serious hardware is so hard to finance.

A purchase order can price parts. It cannot price process learning. A bank can lend against receivables, inventory, equipment, or a creditworthy customer. It cannot easily lend against the fact that a supplier just learned how to make a new kind of module at acceptable yield. Equity investors can fund a brand. Industrial policy can fund a sector. But there is almost no ordinary financial object called a supply chain.

This is strange because, in manufacturing, the supply chain is often the more important unit of analysis.

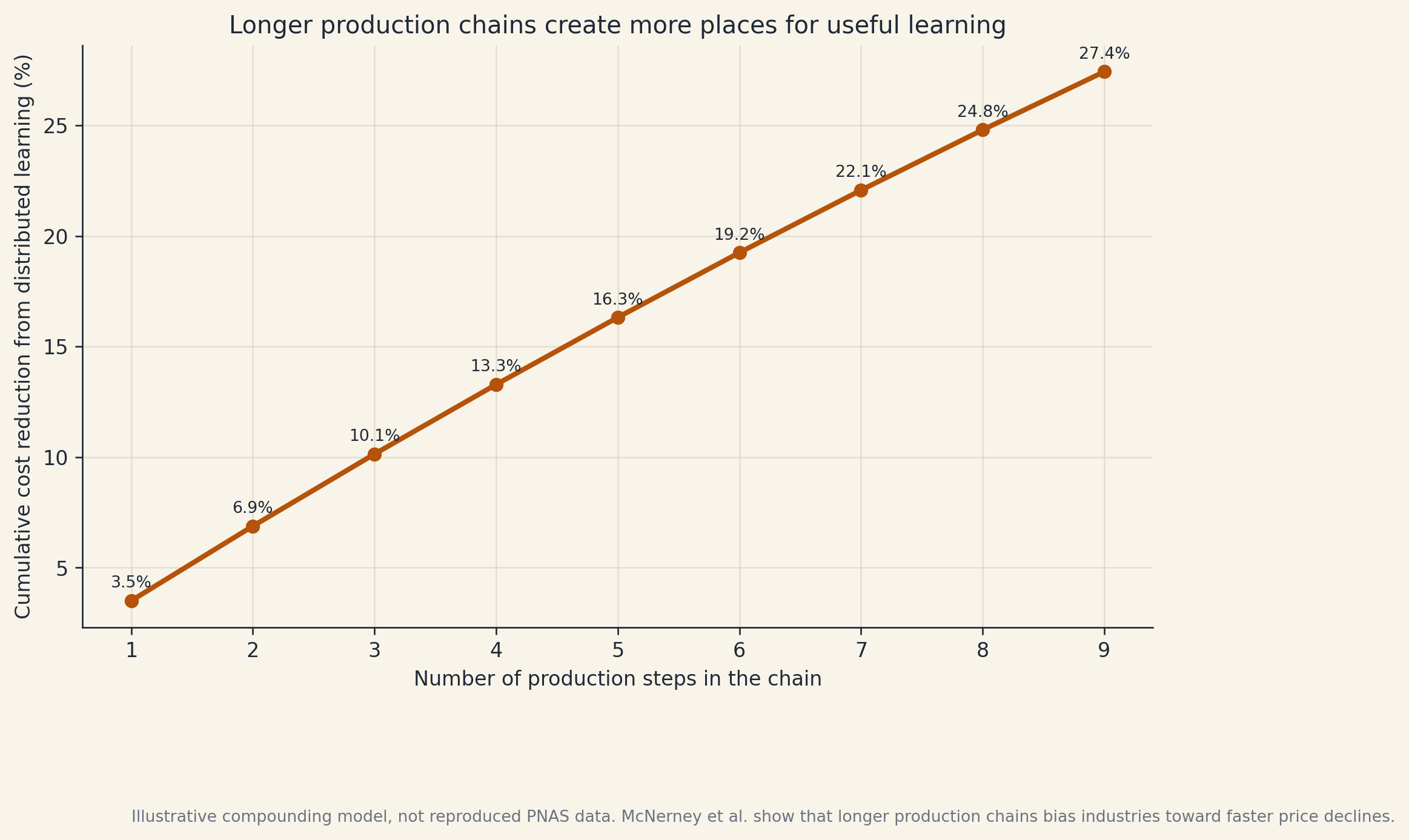

James McNerney, Charles Savoie, Francesco Caravelli, Vasco Carvalho, and Doyne Farmer make a related point in How production networks amplify economic growth. Their model and evidence suggest that production networks amplify technological improvement as it travels through chains of production. Longer production chains bias industries toward faster price reduction, and longer production chains at the country level bias countries toward faster growth.1 Harvard's Growth Lab summarized the result more plainly: longer supply chains and deeper production networks can magnify the benefits of innovation.2

The intuition is obvious to anyone who has stood near a line during ramp. A longer chain is not just more vendors. It is more surfaces for learning. More test fixtures. More tooling tricks. More process windows. More people who discover that the drawing is legal but the part is stupid. More places where a two percent improvement can be inherited by everyone downstream.

Longer production chains create more places for useful learning.

The market understands the firm. It does not understand the chain. That is the financing gap.

Forward Revenue Finance is an attempt to make the chain financeable.

The contract primitive

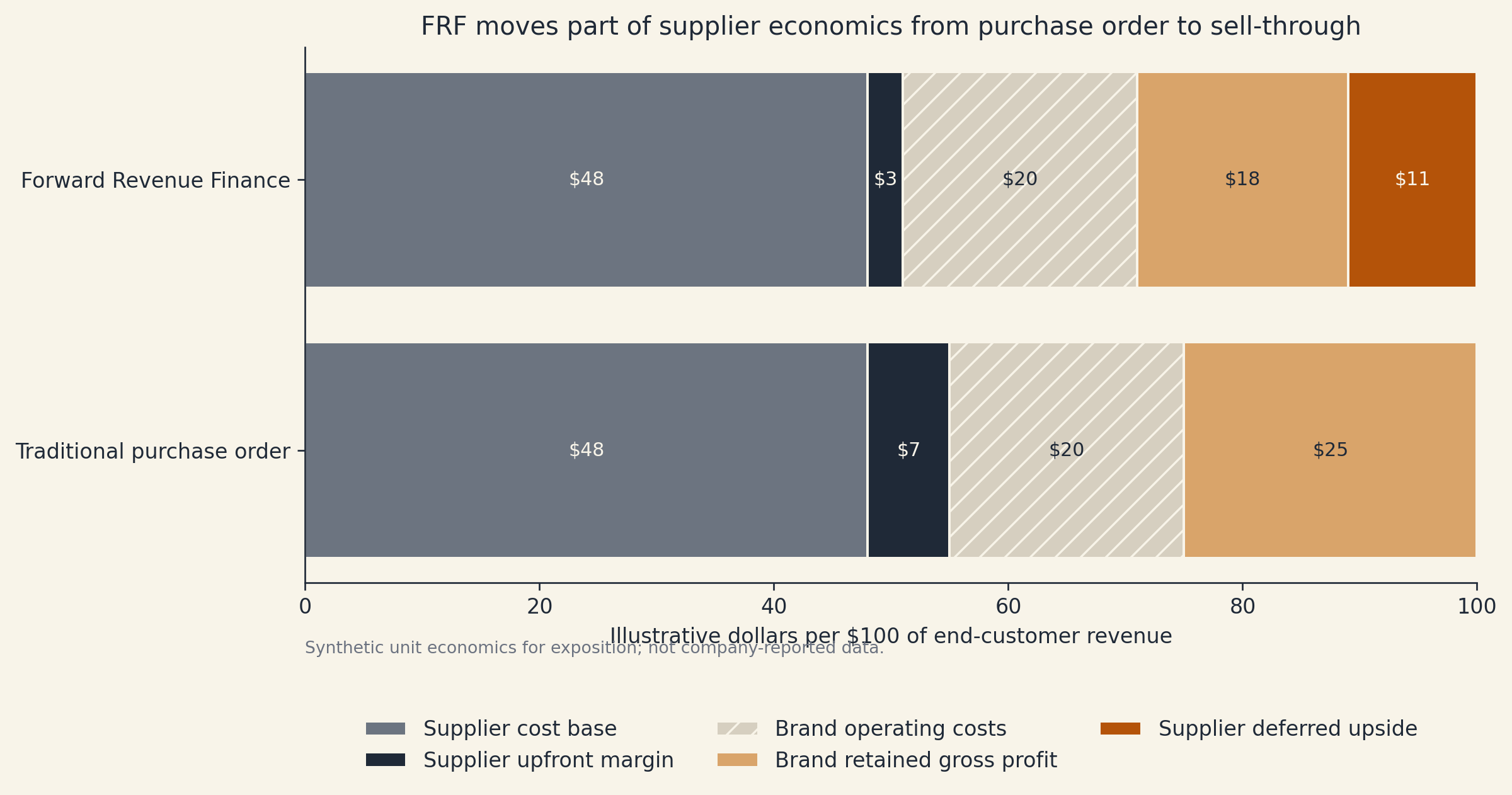

Forward Revenue Finance, or FRF, is a supply contract where a supplier forwards material, capacity, components, integration work, or manufacturing effort to a branded product company at a lower upfront transfer price. The supplier then receives a deferred claim when the final product sells.

The supplier is not merely selling parts. It is financing part of the product's path to revenue.

The brand is not merely delaying payment. It is giving the supplier a defined claim on sell-through.

The bank is not buying venture equity. It can buy or lend against a bounded, auditable production claim.

A clean FRF structure has five parts.

First, the brand pays an upfront supply price at shipment or acceptance. This can be verified cost plus a thin floor margin. The supplier should not be asked to run the line at a loss unless the contract is explicitly underwriting that risk.

Second, the supplier receives a deferred claim tied to sell-through. The claim can be a per-unit kicker, a percentage of net receipts, a margin step-up after channel sale, or a structured note backed by program revenue.

Third, the claim vests against operating gates. The supplier does not earn upside merely because the product sells. It earns upside because it hit yield, quality, delivery, ramp, field reliability, and engineering-support gates.

Fourth, the contract holds a warranty and returns reserve. Hardware has too many ways to lie. A unit can pass outgoing inspection and still fail in the field. The deferred margin should survive only after the defect curve behaves.

Fifth, the program has a ledger. Serial numbers, accepted units, channel inventory, returns, distributor reports, customer receipts, ECOs, warranty events, and payment waterfalls need to be visible enough that a third party can audit them.

This is not factoring. Factoring accelerates an invoice. FRF deliberately delays part of the supplier's economics until the final product proves itself.

This is not pure consignment. Title to inventory matters, but it is not the main point. The main point is that the supplier's margin curve follows product reality.

This is not venture capital. The supplier does not need a claim on the whole company. It needs a claim on the product program whose manufacturability it helped create.

FRF moves part of supplier economics from purchase order to sell-through.

The purchase-order model compresses supplier contribution into a fixed margin. The supplier's best case is getting paid. The brand's best case is a hit product. FRF changes that payoff surface. The supplier accepts lower upfront economics and gets paid more only if the product clears the market and survives the field.

That is not generosity. It is better pricing of risk.

Why the firm is the wrong boundary

The modern economy mostly finances firms, not supply chains.

That is convenient for accountants. It is not how hardware capability actually compounds.

A supplier can develop a process that helps the first customer, the second customer, and a future customer that does not yet exist. A brand can benefit from a supplier's process learning without owning it. A bank can finance the supplier's equipment but not the operating learning that makes the equipment useful. The public benefits when the supplier becomes more capable because future entrants can rent that capability.

This is a positive-sum event with no clean owner.

That is why these events often become either underfunded or politicized. If the spillovers are large and no private balance sheet captures them, the usual solution is industrial policy: grants, loan guarantees, tax credits, local-government subsidies, export-credit support, procurement preferences, or state-directed lending. Those tools can work. They also require the state to decide where the future is.

The alternative is not "let the market solve it," because the current market architecture often cannot see the asset.

The asset is not a factory. The asset is a factory plus a learning curve plus a customer program plus a supplier network plus the option value of future product families.

That object is hard to finance because it sits between firms.

FRF tries to put a security around the part that can be measured: future receipts from products enabled by supplier work. It does not capture every spillover. It does not need to. It only needs to capture enough of the shared upside that private capital has a reason to fund learning before the state has to step in.

The incumbent capacity loop

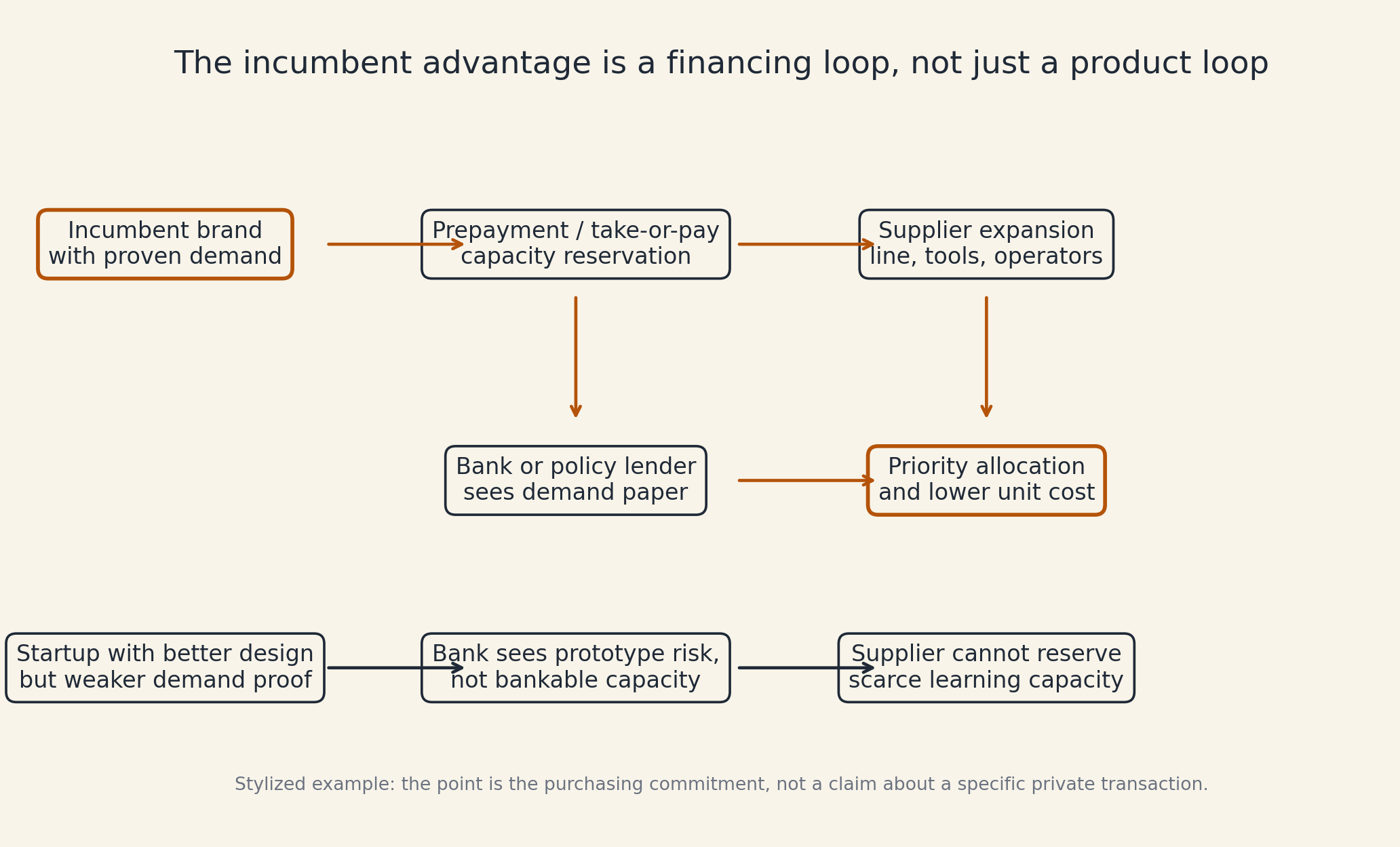

A competitive team can leave Apple or Tesla. The purchasing power does not leave with them.

This is the incumbent advantage that hardware founders underestimate. The issue is not only that Apple has better operations or that Tesla has more factories. The issue is that an incumbent can turn demand certainty into supplier financing.

Apple publicly says its supply chain includes thousands of supplier facilities in more than 60 countries.3 In fiscal 2025, Apple reported products gross margin of 36.8 percent.4 Tesla says its products use parts sourced from thousands of suppliers globally and describes vertical integration and supply-chain localization as part of its competitive strategy.5 Tesla reported 17.8 percent total automotive gross margin in 2025.6

The public numbers are not the important part. The important part is what scale does to the financing loop.

A large incumbent can go to a memory supplier, display supplier, battery supplier, casting supplier, camera module supplier, or advanced packaging supplier and say: expand this line; here is the capacity reservation; here is the purchase schedule; here is the prepayment; here is the volume commitment; here is the reason your lender should believe this capacity will be used.

The supplier can then walk into a bank, a policy lender, or a regional development office with real demand paper. The loan is easier. The expansion is easier. The jobs story is easier. The incumbent gets priority allocation and often better unit economics because it helped de-risk the expansion.

A startup cannot reproduce that loop, even if the actual design team is better.

A group of ex-Apple engineers can have a better product architecture and still be a worse credit signal. A group of ex-Tesla manufacturing engineers can understand the line better and still be unable to reserve capacity. The supplier may like them. The bank may not care. The local government may not care. The capacity will go to the customer whose demand is financeable.

The incumbent advantage is a financing loop, not just a product loop.

This is why vertical integration is so hard to attack from below. Vertical integration is not just ownership. It is a way to keep the returns from process learning inside a balance sheet that capital already understands.

FRF is a way to attack the same problem without forcing every new hardware company to become vertically integrated.

What banks are missing

Modern finance is deeply involved in hardware after the work becomes legible.

Banks finance receivables. They finance inventory. They finance equipment. They finance buildings. They finance acquisitions. They finance finished companies.

They are much less involved in industrial process learning.

That is not because bankers are stupid. It is because process learning has bad collateral shape. Before the line is stable, the asset looks like expense. Before customers pay, the production claim looks like optimism. Before warranty data exists, the yield curve is half evidence and half prayer.

FRF gives banks a better object.

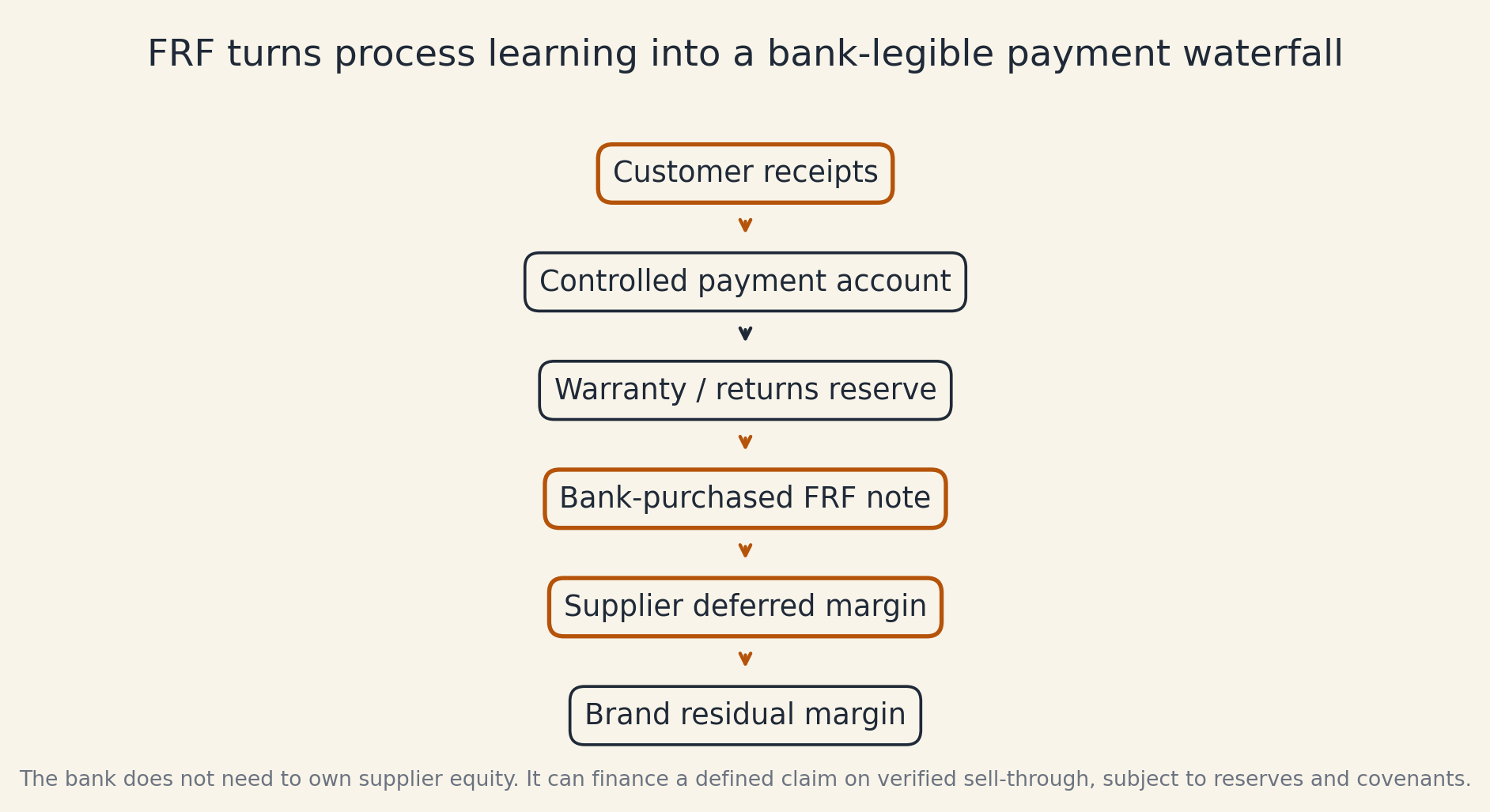

A bank does not need to become a manufacturing expert at the level of the line engineer. It needs the learning curve to be translated into a payment waterfall with covenants, reporting, reserves, and priority. The bank can buy a slice of the forwarded revenue claim or lend against it. The supplier receives cash while operators, technicians, manufacturing engineers, quality engineers, and test engineers are being paid. The brand preserves cash before sell-through. The bank owns a defined claim on product receipts rather than common equity in a startup.

FRF turns process learning into a bank-legible payment waterfall.

This matters because fiat money systems are built around credit creation. The Bank of England's explanation of modern money creation is useful here: most money in the modern economy is created when commercial banks make loans, not by banks simply relending a fixed pile of prior deposits.7

In loose language, people call that "printing money." In banking language, it is credit creation subject to capital, solvency, regulation, interest rates, and credit demand. It is not free money in the moral sense. It is not free money in the risk sense. But it is money that can be created against a credible asset.

FRF says: make industrial learning into a credible asset.

The bank does not have to buy the supplier. It does not have to pick the winning brand. It does not have to pretend that a prototype is collateral. It can finance a production claim with a defined waterfall:

- customer receipts enter a controlled account;

- taxes, shipping adjustments, returns, and warranty reserves are deducted;

- bank principal and coupon are paid if the bank financed the FRF claim;

- the supplier receives deferred margin;

- the brand keeps the residual.

That structure is not exotic. It is ordinary credit discipline applied to a less ordinary asset.

The hard part is data. The bank needs to see enough of the program to know whether the claim is real: accepted units, sell-through, returns, field failures, inventory aging, ECO history, and the difference between channel stuffing and actual demand. Once that ledger exists, the learning curve becomes less mystical.

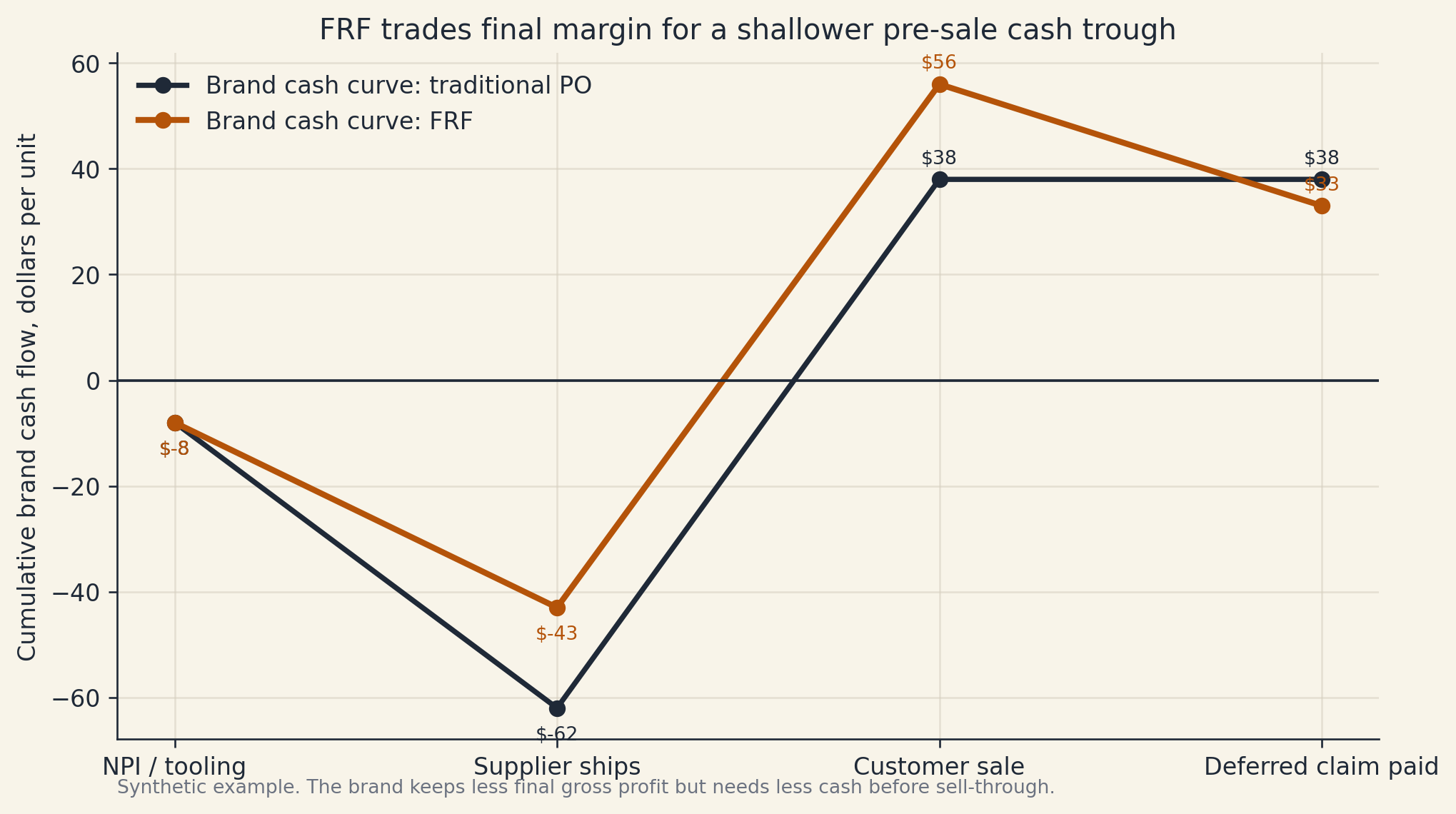

The cash trough

The hardest part of a hardware startup is not the prototype. It is the cash trough between "works once" and "ships repeatedly."

The brand needs money for tooling, long-lead parts, certification, test fixtures, logistics, scrap, pilot builds, engineering travel, quality containment, warranty reserves, and inventory. The supplier needs money for operators, fixtures, capacity reservation, input inventory, yield loss, expedite fees, and the engineering time required to make the line behave.

In a normal purchase-order relationship, both sides try to push the trough onto the other side. The brand wants longer payment terms. The supplier wants earlier payment or higher margin. The stronger party wins. The product does not necessarily get better.

FRF makes the cash trough explicit. The brand trades some final gross margin for less pre-sale cash burn. The supplier trades some fixed margin for a better claim after sell-through. A bank or credit fund can step in because the claim is structured.

FRF trades final margin for a shallower pre-sale cash trough.

This is not appropriate for every part. Commodity inputs should usually stay commodity inputs. FRF is for bottleneck suppliers: the firms that change yield, ramp rate, reliability, cost-down velocity, or feasibility.

The more the supplier is actually co-producing the product's possibility, the stronger the case for FRF.

The invisible giants

Every strong hardware ecosystem has invisible giants.

They are not consumer brands. They are not usually valued like software companies. They may be family-owned, founder-operated, regionally embedded, and allergic to investor theater. But they know how to make difficult things repeatably.

These are the firms that should become stronger if North America wants a thicker hardware supply chain.

The goal is not to turn every supplier into a brand. Many should not become brands. Branding is its own disease. The goal is to let suppliers earn more from the process capability they already create.

Under cost-plus contracting, a supplier's competence often becomes a bargaining disadvantage. The better the supplier gets, the more the customer asks for cost-downs. The customer captures the upside as margin, market share, or faster launch. The supplier gets volume, but not always enough surplus to invest in the next capability.

FRF changes the question from "how cheap can you quote this part?" to "how much of the product's success came from making this manufacturable?"

That is the question the market should want answered.

A thick supply chain lowers the threshold for new branded-product companies. When the chain is thin, only firms with enormous balance sheets, state support, or extraordinary pain tolerance can launch serious hardware. When the chain is thick, a new company can rent more of the world's manufacturing memory.

That is how more Apples and Teslas emerge. Not by copying their org charts. By making the external market behave less like a spot market for parts and more like a compounding base of process capability.

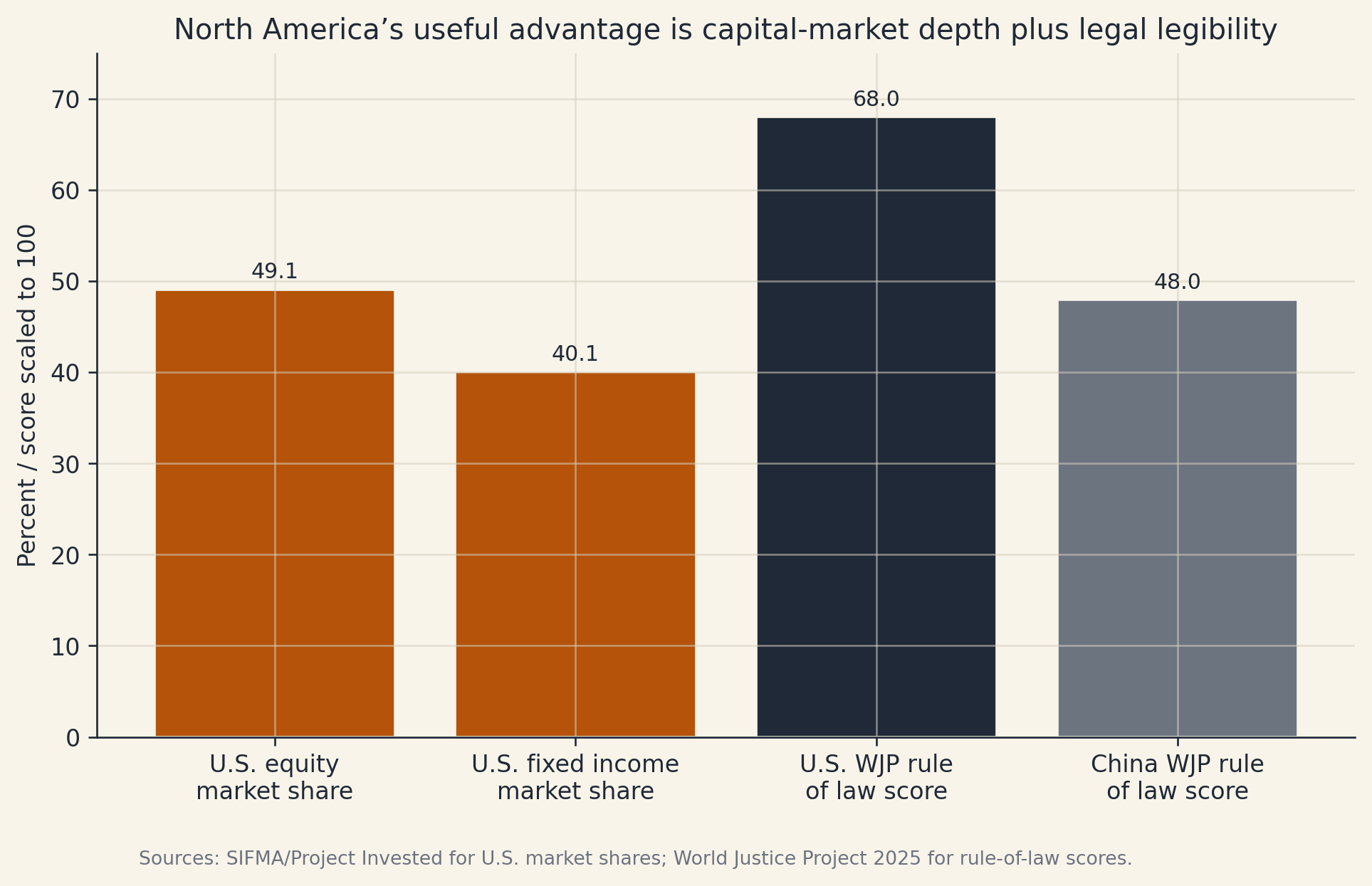

Why this fits North America

China's industrial system is good at coordination. It can use state banks, local governments, land, procurement, subsidies, and directed capacity to solve problems that private contracts in the United States often leave unfunded.

North America should not try to copy that system exactly. It has different advantages.

The United States has unusually deep capital markets. SIFMA's Capital Markets Fact Book, summarized by Project Invested, describes U.S. capital markets as the largest in the world and among the deepest, most liquid, and most efficient; it reports U.S. equity markets at 49.1 percent of global equity market capitalization and U.S. fixed-income markets at 40.1 percent of global securities outstanding.8 On rule-of-law benchmarks, the World Justice Project's 2025 index ranks the United States 27th out of 143 countries with a 0.68 score, while China ranks 92nd with a 0.48 score.9

Those facts suggest a different industrial strategy: do not centralize every production decision; make more production decisions financeable.

North America's useful advantage is capital-market depth plus legal legibility.

FRF is attractive because it uses what North America is already good at: contracts, audit rights, secured credit, covenants, receivable structures, payment waterfalls, specialized lenders, and owner-operator flexibility.

A smaller supplier does not have to become a ward of the state. A smaller brand does not have to raise a huge equity round just to finance inventory and process learning. A bank does not have to pretend it understands every manufacturing detail. Each party needs enough data to underwrite its part of the risk.

This enables coordination without a central planner.

Not perfect coordination. Not frictionless coordination. But more search.

More suppliers can try process improvements. More brands can attempt hard products. More banks can finance bounded claims instead of only finished companies. More owner-operators can remain independent while still accessing growth capital. More experiments can happen in the possibility space between "prototype" and "factory."

Complexity does not emerge because a committee planned it. Complexity emerges because enough capable actors can afford to try.

Failure modes

FRF can fail in obvious ways.

The brand can hide sell-through by manipulating channel inventory, bundling, rebates, transfer prices, or returns. The supplier can chase upside by shipping marginal units. The bank can underwrite paperwork instead of production reality. The contract can turn engineering changes into financial trench warfare. The warranty reserve can be too small. The program ledger can be fake. The startup can die before the product clears the market.

These are not reasons to avoid the instrument. They are reasons to design it like hardware people design everything else: assume the failure modes are real.

The contract needs audit rights. It needs a controlled payment account. It needs field-failure triggers. It needs step-downs for missed yield, late delivery, and quality escapes. It needs inventory aging rules. It needs a treatment for bankruptcy. It needs a sunset. It needs a cap. It needs to distinguish real customer sell-through from stuffing the channel.

Most importantly, it needs engineering governance. If every ECO changes the economics, nobody will tell the truth. FRF works only if the operating gates are objective enough that engineers can keep solving the product instead of negotiating the spreadsheet.

The thesis

The purchase order is too thin a contract for hard products.

It prices units. It does not price process memory. It prices delivery. It does not price yield learning. It prices today's cost. It does not price the supplier's role in making the next million units possible.

Vertical integration solves this by moving the boundary of the firm.

Forward Revenue Finance solves it by changing what crosses the boundary.

The supplier forwards capacity, work, and learning before the product has fully proven demand. The brand forwards part of the future revenue after demand is proven. The bank forwards credit against a structured claim rather than waiting for the learning to become a conventional receivable. The market gets a thicker supply chain without requiring the government to plan every node.

This is the important part: the supply chain itself becomes more bankable.

Not the supplier alone. Not the brand alone. The relationship. The program. The chain of production that creates the product and preserves the learning for whatever comes next.

The invisible giants should not remain invisible in the margin structure.

They should be paid for the future they make manufacturable.

Sources

Footnotes

-

James McNerney, Charles Savoie, Francesco Caravelli, Vasco M. Carvalho, and J. Doyne Farmer, "How production networks amplify economic growth," PNAS 119(1), e2106031118. The arXiv abstract states that longer production chains bias industries toward faster price reduction and countries toward faster GDP growth. arXiv:1810.07774 ↩

-

Harvard Growth Lab summary of the PNAS study. Growth Lab news post ↩

-

Apple, "Supply Chain Innovation." apple.com/supply-chain ↩

-

Apple Inc. 2025 Form 10-K, gross margin table showing 36.8 percent products gross margin in 2025. Apple 10-K (PDF) ↩

-

Tesla, Inc. 2025 Form 10-K, supply-chain description and vertical integration/localization discussion. Tesla 10-K on SEC ↩

-

Tesla, Inc. 2025 Form 10-K, gross margin table showing 17.8 percent total automotive gross margin in 2025. Tesla 10-K on SEC ↩

-

Bank of England, "Money creation in the modern economy." BoE Quarterly Bulletin ↩

-

Project Invested / SIFMA Capital Markets Fact Book summary. projectinvested.org ↩

-

World Justice Project Rule of Law Index 2025, United States and China country pages. ↩